Q&As

QI am not a fan of fund managers. They do nothing but take fees.

In the last six months I’ve been managing my own funds. I feel sorry for those who put money into managed funds. Let me show my investments. Anyone can do this.

AWith your email, you sent a list of six shares, mostly huge multinational companies. And your gain that day was 1.5 per cent — which is fantastic!

If you could get that return every day, after a year $1,000 would turn into almost $230,000. Keep that up and you’ll be a billionaire in no time.

But I don’t like your chances. While having six shares is a lot better than having just one or two, you are still seriously undiversified. If one or two of your companies start to perform badly, you could easily face losses.

What’s more, all your shares are in technology companies. Don’t you remember the Dotcom Bubble? From 1995 to 2000, the technology-heavy NASDAQ share market index rose more than five-fold. Exciting! Then, within a couple of years, it was back to its 1995 level, and many companies in the index had gone broke.

Concentrating on any single industry is not wise — and the volatile technology industry is particularly risky.

I would strongly suggest you spread your money over more shares, and in a wide range of industries.

And once you’ve done that, leave it alone. Research shows that investors often do worse than the share market indexes because they keep trying to pick winning shares and trying to time markets, and often they get it wrong.

As Nobel-winning economist Gene Fama has put it, “Your money is like a bar of soap. The more you handle it, the less you’ll have.”

Meanwhile, I will continue to be one of those people you feel sorry for, who invest in managed funds. And I recommend that to others. Why?

- You get much wider diversification than you can with individual shares. That lowers risk without reducing average returns.

- You can easily deposit and withdraw small or large amounts, and many fund managers let you set up regular deposits or withdrawals.

- The maximum tax is 28 per cent, because the funds are PIEs — portfolio investment entities.

- You can set and forget your investments — changing them only when you need to reduce risk because you expect to spend the money soon. Dividends, tax and so on are taken care of.

The downside is, of course, fees. But you can choose low-fee funds, whose charges don’t eat into returns much.

For you, maybe the second point above is not an issue. And the last point may be a negative. It sounds as if you enjoy watching your investments. Fair enough. But please diversify, don’t trade often, and don’t invest next week’s grocery money.

QPeople are dipping into KiwiSaver to pay for emergency use! Maybe it’s time for people to put aside 1 to 2 per cent of their money and invest it in non-KiwiSaver accounts.

AYes, the increase in financial hardship withdrawals from KiwiSaver is worrying. Too much of that, and people will end up struggling financially in retirement.

Inland Revenue recently said 2,800 people took this step in October, compared with 1,570 in October last year. And the total amount withdrawn more than doubled.

It would be great if everyone set up rainy day accounts. But those who have bitten into their KiwiSaver balances are unlikely to be lining up to do that any time soon.

Perhaps people need a nudge. A great way to do that would be to set up KiwiSaver “sidecar accounts”. This was a recommendation in the 2019 Review of Retirement Income Policies from the Retirement Commission — which, I should declare, I worked on.

The idea is that employee members of KiwiSaver would contribute an extra 1 per cent of their pay, unless they opt out. That money is put into an emergency fund of up to $3,000, within their KiwiSaver account, which the member could access when they need to. Withdrawals would be much easier than hardship withdrawals.

Once the $3,000 is reached, the extra money would go into the person’s ordinary KiwiSaver account. If they withdrew any sidecar money, the extra 1 per cent would replace it until the sidecar reaches $3,000 again.

At the time of withdrawal, the member would be offered help with running their finances — in the hope they wouldn’t need to keep emptying their sidecar.

The beauty of this idea — as opposed to simply encouraging everyone to set up rainy day money — is that it would happen automatically. But if anyone really didn’t want to do it, they wouldn’t have to. Joining KiwiSaver, itself, operates that way, with non-members auto enrolled when they get a job but allowed to opt out. That is surely one reason the scheme is so widespread.

I reckon most people would like the sidecar idea. After all, 1 per cent of your pay, if you earn $50,000 a year, is less than $10 a week. On $100,000 it’s less than $20 a week.

The upshot: fewer KiwiSaver retirement accounts would be raided in hard times.To those who say KiwiSaver should be for retirement only, this change would mean more savings would make it to retirement.

I actually wrote about this back in April. At that time MBIE said they were looking into “potential enhancements to KiwiSaver”. How about sidecars, new Government?

QI own one property, a rental unit in Auckland. The current value of the rental unit is about $750,000, and it has $150,000 left on the mortgage (with six years left to pay it off), leaving about $600,000 in equity.

The rental is a 1970s concrete block unit and will require significant maintenance in the coming years as well as the usual ongoing costs and interest.

My partner and I live in in Christchurch and are currently renting, as we’re not sure where we want to live longer term.

Would it be worth looking at selling the unit and buying another new-build rental for $600,000 in Auckland or elsewhere, and therefore having no mortgage? Rental income (after expenses) could then go into an investment fund.

ANobody knows which option will make you better off. Trying to forecast returns on property and the shares and bonds in a fund is impossible.

But I can see several advantages in your selling plan:

- Paying off a mortgage is never a bad move, and it’s particularly effective given current interest rates. If you’re paying, say, 7 per cent, getting rid of the mortgage will improve your wealth as much as earning 7 per cent, after fees and tax, on an investment, risk-free. That’s pretty good.

- You would be diversifying beyond property — although I hope you are already in KiwiSaver.

- You could buy a rental unit in Christchurch — or wherever you are most likely to end up. It usually works better if you live near a rental property, especially if things go wrong with either the building or the tenants.

- You could invest the net rental income in a fund at the appropriate risk level, depending on when you’re likely to buy your own home.

If that might happen within a few years, I suggest you use a conservative fund. Your average returns won’t be as high as in a higher-risk fund, but there’s less chance you’ll be hit by a market downturn when you want to buy.

But if a home purchase seems to be quite a few years away, you could go with a balanced or growth fund, and lower your risk as you approach buying time.

QWhy wouldn’t the Government and the Reserve Bank consider raising compulsory saving in KiwiSaver as an alternative to raising interest rates, with a view to lowering inflation?

Both take money out of circulation, but raising interest rates only serves to enrich Australian-owned banks, while raising compulsory saving levels keeps the money here in NZ and could be used to invest locally as well.

Certainly, it would be a much easier sell if citizens know the money will be there for them at a later date, rather than in the pockets of wealthy offshore investors.

AI like the creativity of your idea. And another reader with a similar suggestion makes a further point.

Raising the KiwiSaver contributions rate “might have the effect of reducing spending ability for everyone in the country more immediately (rather than just mortgage holders and only then at the end of their fixed term period),” he says. “It seems then everyone suffers hopefully a little less for a shorter time.”

However, I’m afraid I’m going to be a wet blanket.

Firstly, the Government would have to support it, as the Reserve Bank doesn’t set KiwiSaver policy.

To be fair, it would have to make KiwiSaver compulsory for everyone — which would hit those not currently in the scheme or not contributing, including many going through hard financial times.

I appreciate that raising mortgage rates affects only some people, but they would tend to be better off than people not in KiwiSaver.

But let’s assume, for the moment, that the Government likes the idea. Does the Reserve Bank think it would work?

“While changes in the OCR (official cash rate — the Reserve Bank’s interest rate) are ultimately linked with the amount of money in circulation, the main way these changes affect economic activity is through altering the incentives individuals face, now and in the future,” says a spokesperson.

“For example, a higher interest rate today encourages households to save more and consume less, with flow-on effects to soften overall economic activity and inflation.”

It’s important to note, he says, that “individuals are still able to react to changing interest rates in whatever way they feel is best: for example, some may still choose to borrow at higher interest rates if they find themselves in a position to do so.”

By contrast, your idea would be ordering people to change their retirement savings.

“In reality, it is likely that people will simply reallocate from other forms of saving into KiwiSaver (as directed), rather than necessarily increase their savings overall. This would reduce the policy’s effectiveness,” says the spokesperson.

Of course that’s true only to the extent people also save outside KiwiSaver, but I suppose many do.

He goes on to say the Reserve Bank can use a wide range of “channels”, including “variable tax rates, lump sum transfers, retirement schemes, sovereign wealth funds and others.”

But “Experience within New Zealand, as well as through much of the developed world over the past several decades, strongly suggests that there is a robust channel from changes in the OCR through to inflation. Monetary policy can best promote overall welfare by using this channel to maintain low and stable inflation.”

He acknowledges that “higher interest rates will make borrowers worse off.” But there are other ways a government can compensate for that if it wants to.

“Monetary policy is working, as expected, to lower inflation. We remain confident that CPI inflation will return to the 1 to 3 per cent target band by late 2024, and to 2 per cent in 2025.”

Hang in there, people with mortgages.

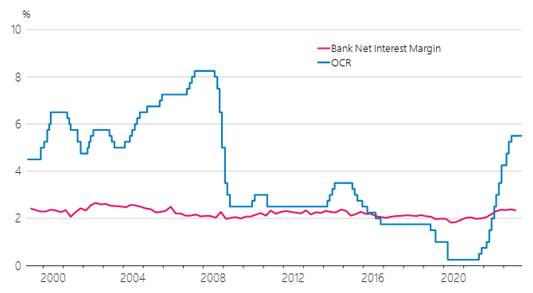

On your point about raising interest rates enriching Australian-owned banks, the spokesperson says, “Increases in the OCR do not on their own increase bank profits.”

That’s because banks change their deposit rates as well as their mortgage rates. The difference between the two is called a bank’s net interest margin.

“In the most recent tightening cycle, lending rates have risen faster than banks’ average deposit funding costs, giving a temporary boost to banks’ net interest margins, which are a large component of their profits. However, we saw the opposite in early 2020, when banks’ interest margins fell.”

Bank profits don’t change with interest rates

Source: Reserve Bank of NZ

Over the longer term, as the graph shows, “banks’ net interest margins have been relatively stable, despite large cycles in monetary policy and the OCR,” says the spokesperson.

In the end, then, changes in interest rates don’t tend to enrich banks. Instead, when rates rise, money is transferred from those with mortgages to those with bank savings and term deposits. And when rates fall, the flow goes the other way and savers are worse off. Broadly speaking, the money stays in this country.

No paywalls or ads — just generous people like you. All Kiwis deserve accurate, unbiased financial guidance. So let’s keep it free. Can you help? Every bit makes a difference.

Mary Holm, ONZM, is a freelance journalist, a seminar presenter and a bestselling author on personal finance. She is a director of Financial Services Complaints Ltd (FSCL) and a former director of the Financial Markets Authority. Her opinions are personal, and do not reflect the position of any organisation in which she holds office. Mary’s advice is of a general nature, and she is not responsible for any loss that any reader may suffer from following it. Send questions to [email protected] or click here. Letters should not exceed 200 words. We won’t publish your name. Please provide a (preferably daytime) phone number. Unfortunately, Mary cannot answer all questions, correspond directly with readers, or give financial advice.