Q&As

Where’s all the cheering?

QI have $40,000 in my balanced KiwiSaver account with the BNZ. I turn 65 next February and wonder if it would be better to withdraw the money then and put it on term deposit where I can get 6.10 per cent. I won’t need to use it for quite a while as my husband is still working.

Part of my reason is that I understand term deposits and can see my money increasing, which is comforting. I don’t have a clue how my KiwiSaver works, try as I might to understand it. It looks as though I’m just losing money, and at my age that’s not a good feeling.

ARelax. And smile! On BNZ’s website its KiwiSaver Balanced Fund reports a return of 1.68 per cent in just the last full month — February. Over six months the return is 6.61 per cent, and over the 12 months ending February it’s 12.17 per cent. Impressive numbers.

Not that your fund is particularly special. The average KiwiSaver balanced fund return was 11.8 per cent in the 2023 calendar year, reports Morningstar. Pretty much all balanced funds — and all KiwiSaver funds at all risk levels actually — have done really well lately.

The average conservative fund return was an astonishing 8.2 per cent last year. For moderate funds it was 8.8 per cent, for growth funds 13.2 per cent, and for aggressive funds 15.5 per cent.

So where’s all the cheering? There are plenty of complaints when KiwiSaver funds perform badly. But terrific returns go unheralded.

Of course, we shouldn’t take too much notice of short-term returns, which can be all over the place. Indeed, your fund’s return in the year ending March 2023 was minus 2.37 per cent, according to the Smart Investor tool on sorted.org.nz. And the fund had tiny returns in two other recent years — countered by a whopping 16.71 per cent in the year ending March 2021, as the markets recovered from the Covid downturn.

It’s much wiser to look long term. And in the ten years ending December 2023, your fund’s average return was 6.4 per cent, says Morningstar. That places it sixth out of 16 balanced funds that have been around that long.

Meanwhile, six-month term deposit rates were around 4 per cent ten years ago, but dropped to less than 1 per cent by 2021, and have only recently risen to around 6 per cent. Your fund has done way better than that.

But enough chiding! You — and everyone else in KiwiSaver — have had an up-and-down ride since 2020. Perhaps it’s made you reluctant to check how your fund is doing, for fear it would be bad news.

The question now is: What should you do when you get access to the money early next year?

Your fund invests about 60 per cent of its money in shares, 35 per cent in bonds and 5 per cent in cash. Over long periods it should pretty much always outperform term deposits, but with ups and downs.

If you really can’t cope with declines, you could switch to a lower-risk fund now, just by asking BNZ. And once you’re 65, you could switch to term deposits if you prefer them. However, don’t count on their high rates continuing. All the experts are predicting rate falls.

P.S. On how a KiwiSaver fund works, the shares it holds bring in money through rising share values as companies grow, and through dividends paid from company profits. And bonds and cash are rather like term deposits in that the fund receives interest — although it can also make money by selling bonds at a profit.

Missing out

QI contacted you a few years ago after receiving an inheritance, and duly read your book “Rich Enough?” I have invested my money in a fund using InvestNow.

I started with about $30,000 each month until about 4–5 months in, where I was too disheartened by the state of the markets! I put the rest into term deposits in the interim, as the interest rates were starting to look good.

Recently my stocks returned to their original values so I’ve resumed my contributions. I appreciate that this goes against your advice about continuing to drip-feed, but… it was a struggle to see them going down down down.

AGood choice to got into a fund, and it sounds as if it’s largely invested in shares. Over the long term you should do well.

But you broke a “rule” — stopping your regular investments when the markets fell. That’s a pity. With the value of units in your fund lower than usual, every dollar of your new contributions would have bought more units. Then you could have watched the unit value rise as the markets recovered — which always happens in the end, even if it takes a long time sometimes.

Meanwhile, of course, the value of the money you had invested earlier went down. That’s no fun to watch. But whenever you keep investing a regular amount, buying bargains is one consolation of a downturn.

Also, trying to time markets is a mug’s game. They can rise suddenly, leaving the sideline sitters out of the action. Lots of research shows those who try to time their buying and selling tend to do worse than the steady investors. And it’s much easier if you just ignore market movements!

Ladder for the long term

QJust read in your last column about the person who laddered investments on 5-year terms. Perhaps 5 years is too long as rates change often. I set up 12 six-month term deposits so I get interest paid about every two weeks, which supplements my Super.

AWhat you’re doing seems to work well for you. But you’re missing some advantages of laddering over longer terms.

As I explained last week, usually banks pay higher interest for longer terms. Although that’s not happening in the current unusual market conditions, it’s sure to return in a while.

Also, if you ladder over terms of, say, three or more years, when rates fall you can comfort yourself that you still have some deposits at the old higher rates for quite a while. And when rates rise, you’ll be glad to have some money maturing fairly soon to get those higher rates. It’s a type of diversification.

By contrast, while your system works well now, you might find that the interest on all your 12 deposits looks pretty unattractive within the next year or two.

What pushes up rents?

QNever believe anyone who tells you rents are related to property value, or the landlord’s outgoings. That’s only in landlords’ dreams.

I’ve been a landlord and tenant at various times in three countries, over more than 50 years, and it’s my experience that rents almost entirely go on supply and demand, for the particular type of property, in the particular location. I’ve had properties where property value doubled or trebled, mortgage interest went up, but rent was static for years, or even went down, and vice versa.

AYou’re quite right. When the Labour Government took away mortgage interest deductions, some landlords said rents would rise because of that. Rents have risen, but was that really the reason? I doubt if we’ll see rents fall when these deductions are reintroduced.

So what does affect how high rents are? Research published last August found that “Wage inflation and relative supply and demand of dwellings (measured by people per dwelling) are the two key drivers of rental inflation for new tenancies at the national level.”

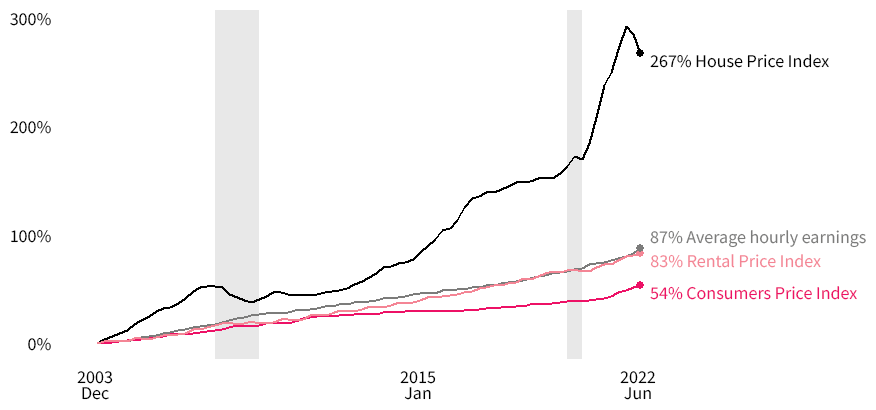

Rent prices have risen broadly in line with wages

Less than house prices, but more than general inflation

Cumulative percent change, since 2003Q3

Shaded areas show recessions

Graph: The Treasury, Ministry of Housing and Urban Development, Reserve Bank of NZ

Data: Ministry of Housing and Urban Development, Stats NZ

In other words, rents are largely decided by how much tenants can afford and how hard it is to find a place to rent. Our graph shows how closely rents follow hourly wages — and not house prices.

The report, from the Housing Technical Working Group, a joint initiative of the Treasury, Ministry of Housing and Urban Development and Reserve Bank, noted that there’s also some correlation between mortgage interest rates and rents, and between unemployment and rents, but those impacts are quite small.

NZ through UK eyes

QMost people seem to look only at how the landlord and tenant are affected when they debate interest tax deductibility. But there is another aspect.

My son works for a very large bank in the UK. His main job is to approve loans to UK companies. As he was born in New Zealand and lived here until his early twenties, it is normal for New Zealand enquiries to be forwarded to him.

When our previous government unilaterally removed interest deductibility in New Zealand my son was forced to tell any UK prospective investors in New Zealand about this.

The response was, “If the government can do this, is there anything to stop them from removing tax deductibility from other things as well?”

What with the various “captain’s calls” being used to justify almost anything being passed under urgency in a pandemic, the answer to that question had to be “no”. This of course very quickly removed any interest in investing in New Zealand by UK business people.

The recent removal of the tax deductibility has renewed interest in investing in New Zealand and is making it easier for overseas investors to do so. Surely that’s a good thing.

AGenerally, overseas investment in New Zealand business is good for our economy. So it’s not wise to discourage it. (Foreign ownership of New Zealand rental property is more worrying, but that’s not what you’re talking about.)

But surely your son could have explained that there was a special reason for disallowing interest deductions on rental property — to try to slow house price rises and make more houses available for first home buyers. There was no suggestion of expanding the change beyond rental property.

On captain’s calls and the pandemic, I would have thought UK investors would have been impressed with our Government’s handling of the crisis. Compared with New Zealand, nearly five times as many people per head of population died of covid in the UK, according to Financial Times data — while their prime minister partied on.

Deductible or not?

QWhen I went to accountancy school (aka university) interest was only tax deductible if the original purpose of the debt was to create taxable income.

I do not believe renting a house you bought (and borrowed money on) to live in as your primary residence is deductible, if you subsequently move out and start renting it.

AYou’re referring to last week’s column, in which I quoted Terry Baucher of Baucher Consulting as saying that if you let out your house and move in with family, 80 per cent of your mortgage interest would be deductible from April 1, and the whole lot from April 1 next year.

Baucher now comments on your letter: “Your questioner is correct in that the purpose matters, but the key phrase in the Income Tax Act is that an expense is deductible ‘to the extent to which the expenditure is incurred in deriving assessable income.’

“So if a person is renting out their home (because they’ve moved to another town for work) the rent is assessable and therefore the interest becomes deductible from the date of rental.”

He continues, “As you covered in the column there is a problem if the owner tries to manufacture a deduction through a non-genuine rental arrangement. Your questioner’s interpretation would be very harsh as it wouldn’t accommodate the many occasions where people move to new towns (or countries) and rent out their former home.”

However, Baucher adds, “Of course being tax law there’s always a little quirk, and the interest would NOT have been deductible if the person had bought their home on or after 27th March 2021 with a mortgage, and then decided to rent it out. (The restrictions on interest deductibility that will cease entirely from 1st April 2025 only applied to existing loans as of 27th March 2021. No deduction was allowable for any new loans after that date).”

Okay, I think we’ve had more than enough on mortgage interest deductions!

No paywalls or ads — just generous people like you. All Kiwis deserve accurate, unbiased financial guidance. So let’s keep it free. Can you help? Every bit makes a difference.

Mary Holm, ONZM, is a freelance journalist, a seminar presenter and a bestselling author on personal finance. She is a director of Financial Services Complaints Ltd (FSCL) and a former director of the Financial Markets Authority. Her opinions are personal, and do not reflect the position of any organisation in which she holds office. Mary’s advice is of a general nature, and she is not responsible for any loss that any reader may suffer from following it. Send questions to [email protected] or click here. Letters should not exceed 200 words. We won’t publish your name. Please provide a (preferably daytime) phone number. Unfortunately, Mary cannot answer all questions, correspond directly with readers, or give financial advice.