Q&As

QI often read your column to get direction on many financial matters. My background in financial matters is limited and I place a lot of weight on your advice.

In last weekend’s Herald, in the business section, I noticed an ad for AE KiwiSaver that has apparently returned 12.5 per cent a year for the last five years.

That is way better than my Simplicity KiwiSaver Growth Fund, but I don’t understand why it is only now I have learned about this company. It also claims to be ethical and appears to be, from looking at their website.

Can you explain why you have not mentioned this company, as it appears to be giving people good returns in a very acceptable style of investing?

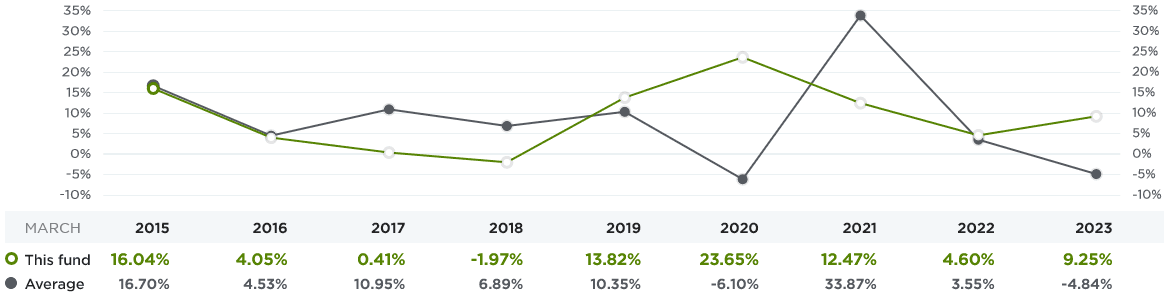

ASomething tells me you wouldn’t have been quite so interested in this provider back in the year ending March 2018, when its return was minus 1.97 per cent, while the aggressive fund average return was 6.89 per cent.

AE KiwiSaver Fund Performance

It sometimes beats aggressive fund average, sometimes not

AE fund in green, average aggressive fund in grey

Over a longer period, the years ending March 2015 to March 2018, the AE fund’s return averaged 4.63 per cent, less than half the average aggressive fund’s return of 9.77 per cent a year, according to data from the Smart Investor tool on sorted.org.nz. All returns are after fees.

Three years later, in the year ending March 2021, their 12.47 per cent return might have caught your eye, but hopefully not. That was the astonishing year that started at the bottom of the Covid stock market plunge and ended in the big recovery, and the average aggressive fund return was 33.87 per cent. In My opinion, AE – which is also known as Always-Ethical,- seriously underperformed.

Okay, I’m picking AE’s bad years. But it seems to me that in the ad AE is cherry picking their good years. Cherry picking is fair enough when you’re choosing which photos to put on social media. But we’re talking about New Zealanders’ retirement savings here.

The Financial Markets Authority has addressed this issue in its Guidance Note on advertising offers of financial products under the FMC Act: “Past performance information must be meaningful and be presented in a balanced way. Data that is “cherry-picked” to create a more favourable impression, or overly reliant on additional information for understanding, may create a misleading impression.”

AE’s CEO, Sandra Clark denies cherry picking. “As far as we are aware the industry norm is to report one-year results, the average of five years and (if available) that of ten years. Unfortunately, Always Ethical is unable to provide ten-year figures as AE has not existed for that long,” she says.

She refers to the FMA’s Guidance Note, which she says “recommends that funds advertise 1-year, 5-years, and if available 10-years, which is what we have done.”

The FMA document actually also includes three-year results. And those don’t make AE KiwiSaver look quite as good. Its three-year average return is 8.77 per cent, compared with the aggressive fund average of 10.86 per cent, Smart Investor data show (See here).

Says the FMA: “For all advertisements that mention performance, regardless of period, issuers should ensure the advertisement is balanced.” Balance seems to me to be lacking in the ad that caught your eye, given that it includes returns from a period of particularly strong performance, and in my view does not reflect AE’s results over shorter or longer periods. I would like to see the ad stopped.

So, to answer your question, I don’t point out KiwiSaver funds that perform unusually well in one period simply because they are just as likely as any other fund to perform badly in the next period — if not more so.

Despite common bad advice, it’s not wise to choose a KiwiSaver fund, or any other investment, based on past returns. Even when the returns do not focus on one period of particularly good performance – if we look at, say, a whole 20 years – research shows that good performers last time are often poor performers next time.

Looking beyond returns, who is AE KiwiSaver, which was formerly known as Amanah? It’s notable for three reasons:

- It is said to be the only Shari’ah-compliant KiwiSaver provider, which means it is suitable for Muslim investors, although all investors are welcome.

Because of this, AE avoids investing in companies “whose return is based on receipt of interest”, including banks and insurance companies. It also avoids companies involved in gambling, alcohol, tobacco, weapons of war, pork, fossil fuel exploration and so on.

However, the provider doesn’t say it avoids companies with bad credentials on animal cruelty. And the Mindful Money website notes that more than 5 per cent of its investments are in two companies with bad records in that area — Pepsico and Albermarle Corp.

Over all, though, the provider does pretty well on “ethical” investing.

- AE has just the one KiwiSaver fund, which invests in US shares — currently 96 per cent of its investments, according to Smart Investor. The rest is in interest-free cash accounts.

The ratio of shares to cash varies depending on the AE investment committee’s assessment of the world economy. But AE recommends that investors treat its KiwiSaver fund as aggressive.

Aggressive funds are the most volatile KiwiSaver funds. They usually perform well over the long term, but short-term losses are also quite common.

Smart Investor shows that AE has, as the ad claims, reported unusually high average returns over the last five years — averaging 12.59 per cent a year, compared to the average for all aggressive funds of 6.67 per cent.

The five-year number is boosted by AE’s extraordinary 23.65 per cent gain in the year ending March 2020, in the depths of the Covid downturn, when the average aggressive fund reported a loss of 6.1 per cent. See graph.

I asked Clark how it did so well at a time when the US share market index was falling.

“We made significant gain from the stock we were invested in through until February 2020,” she says.

“You will recall the US market in March 2020 had a correction. At the time of the correction to reduce volatility on our return (ie the members’ funds), as required by our SIPO (statement of investment policy and objectives), we were holding approximately 25 per cent equities and 75 per cent US currency.

“We therefore retained in cash the performance of the market prior to that adjustment, and with the correction obtained the benefit of the inter-relationship between the US market and the NZ dollar. This is how our product has been deliberately designed.”

I have to acknowledge AE’s timing worked really well that year. But it doesn’t always, as noted above.

Regular readers will know that I don’t think trying to time markets is a good idea — and nor does hugely successful US stock investor Warren Buffett. “We haven’t the faintest idea what the stock market is going to do when it opens on Monday,” Buffett said at his company, Berkshire Hathaway’s 2022 annual meeting. “We’ve not been good at timing.”

- The AE fund charges the highest fee of any KiwiSaver fund in Smart Investor — at 3.03 per cent. This is way above the aggressive fund average of 1.07 per cent.

Says Clark, “We are not a low fees provider as we are not prepared to abrogate our responsibility to some US based analyst, we charge a fair fee.”

The high fee perhaps reflects that it is expensive to make the fund’s ethical checks and to trade frequently. Still, high fees reduce the amount available for investor returns. And, as the FMA puts it, “There is no systematic relationship between fees charged and returns received.”

Meanwhile your Simplicity Growth Fund charges fees of just 0.29 per cent, less than 10 per cent of the AE fee and the lowest for growth funds in Smart Investor. I recommend choosing a KiwiSaver fund — at the right risk level for you — based largely on low fees. Your fund is not a bad choice.

A final comment: It’s great that AE offers a KiwiSaver fund for Muslims, who might otherwise miss the chance to belong to KiwiSaver. But I would like to see Muslims also offered a lower-fee option.

QMy wife and I are both 66. We have a house we live in Auckland and a rental property on the Kapiti Coast. Both are mortgage-free and valued about a million dollars each before the recent downturn.

We are asset rich and money poor. We have $100,000 in the bank, receive our super and get $600 a week rental on the Kapiti property. We like to travel.

Should we sell one of the properties or keep both? Either one would need about $30,000 spent on it before selling it — new roof, paint etc.

Do we get a reverse mortgage to have money for maintenance and travel etc? Do we keep things as they are and use the $100,000 for travel and essential maintenance only? None of the above? Your opinion would be greatly valued.

AMy strong recommendation: spend $30,000 on tarting up the rental property and sell it. That will give you heaps for travel and anything else.

Many people own rental properties in retirement. That’s fine if you have plenty of spending money; no hassles with tenants, maintenance and so on; and you enjoy your role as a landlord.

But — unlike investments in shares, bonds, managed funds and so on — you can’t gradually spend the money tied up in a rental. If you need that money to make the most of life, get out of the rental game.

QI think that if you want to, you can make repayments to Heartland on a reverse mortgage in the same way you would with a normal mortgage. It might not cover all the interest but would reduce the amount that is compounding.

AYou’re right. Heartland Bank’s website says, “You may repay all or part of your Heartland Reverse Mortgage at any time without penalty.” And SBS, the other main provider of reverse mortgages, says,”You can repay the loan, in full or in part, at any time.” More on reverse mortgages next week.

QIn your last column someone asked, “Why did last week’s correspondent waste time with BNZ term deposits when SBS and TSB consistently offer better interest rates?”

I’m the original correspondent. My reply: Because the correspondent already has accounts with BNZ, Westpac and ANZ, and adding two or three more is time wasting for possible marginal gains.

Also because the correspondent notes that SBS is rated BBB and TSB is rated A- while his banks are all AA-. And until the government deposit guarantee kicks in it is safer to stay with the more solid banks.

AFair enough. While it seems unlikely a smaller New Zealand bank will go belly up before the deposit guarantee starts — probably some time next year — we can’t be certain.

The smaller banks’ lower credit ratings suggest they are somewhat riskier than the big banks. For more on bank ratings, see the Reserve Bank website.

A Reader’s Story

Since mid April, to mark the 25th anniversary of this column, we have run some readers’ stories of how the column has helped them over the years. Here’s another.

QI have been an avid reader of your column and visitor to your website for the last 10 years. You have made me understand how important it is to be aware of what is happening to my money, particularly in my KiwiSaver account.

Your sage advice kept me calm when my KiwiSaver savings dropped during the Covid lockdowns as I know that if you have 10 years of working ahead of you, there is plenty of time for it to pick up again. When my KiwiSaver provider asked me last year if I wanted to move to a more conservative account I decided to stay in a balanced account for a few more years.

I have made sure to only have good debt — house and study — and paid off credit cards in full. I’ve increased the amount I pay into my KiwiSaver and on my mortgage as my income has increased. If I ever have enough spare money to start investing, I feel confident that I understand laddering to make the most of those investments.

AWell done. Great that you “survived” the Covid jitters. And I particularly like your increased KiwiSaver and mortgage payments as your pay rises.

No paywalls or ads — just generous people like you. All Kiwis deserve accurate, unbiased financial guidance. So let’s keep it free. Can you help? Every bit makes a difference.

Mary Holm, ONZM, is a freelance journalist, a seminar presenter and a bestselling author on personal finance. She is a director of Financial Services Complaints Ltd (FSCL) and a former director of the Financial Markets Authority. Her opinions are personal, and do not reflect the position of any organisation in which she holds office. Mary’s advice is of a general nature, and she is not responsible for any loss that any reader may suffer from following it. Send questions to [email protected] or click here. Letters should not exceed 200 words. We won’t publish your name. Please provide a (preferably daytime) phone number. Unfortunately, Mary cannot answer all questions, correspond directly with readers, or give financial advice.