Q&As

- KiwiSaver totals over the years should be adjusted for inflation — but let’s not get carried away.

- People receiving ACC payments or Paid Parental Leave have a choice in KiwiSaver.

- Early retirement plans won’t be harmed by membership in KiwiSaver.

QThe most annoying thing I find about KiwiSaver promotions is that the dollar numbers given out are not adjusted for inflation.

For example, they may say if you are 35 and join KiwiSaver you may retire with $600,000 in 30 years. But it is absolutely misleading to say that without reminding people that that is in today’s dollars. What will $600,000 be worth in 2037? A lot less than now!

In fact if you go back over the last 30 years and use the Reserve Bank’s own calculator — go to www.rbnz.govt.nz and click on “CPI inflation calculator” — you find you would need $3.73 million in 2007 to buy the same amount of goods that $600,000 would get you in 1977. Prices have increased more than six-fold. Or to put it another way, money has lost 84 per cent of its purchasing power!

Now if we have the same level of inflation over the next 30 years, $600,000 will only be worth about $96,000 in 2037 dollars, in purchasing power.

So it is deceitful of the government to propose what we might have on retirement without talking about inflation adjustments.

I think we are heading into higher inflation times for the next 15 years — to at least the 1970s level.

AYou seem blissfully unaware of Don Brash’s major achievement before he became National Party leader. As governor of the Reserve Bank, he got much of the credit for bringing New Zealand’s inflation dramatically down from the heady 1970s and 80s levels.

And the New Zealand government — like most other developed countries’ governments — is pretty determined not to let inflation run away again. In fact, one of our Reserve Bank’s main functions is to maintain price stability — along with keeping our financial systems running soundly and efficiently, and providing us with cash.

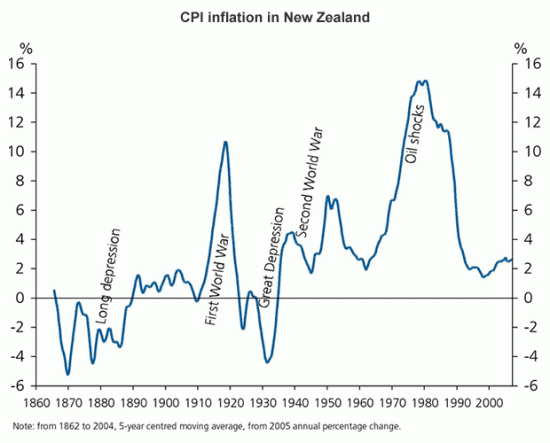

Even if that weren’t the case, it seems unlikely inflation would rise back to 70s and 80s levels. Our graph shows how unusual, historically, those levels were. For the rest of the last 140 years, inflation has rarely topped 5 per cent.

Still, you make a good point. Even with much slower inflation, over long periods it greatly affects purchasing power.

The problem is how to explain this when looking at expected growth of savings. Readers’ letters and conversations reveal that people get confused by what “inflation-adjusted” means.

Perhaps the easiest way is to say that with 2 per cent inflation, the value of your savings — in terms of what you can buy with them — will halve in 35 years. If a KiwiSaver account is expected to grow to $1 million in 35 years, that million dollars will buy what $500,000 buys now.

Why 2 per cent? That’s the current inflation rate. If you want to allow for a bit of upside, with 3 per cent inflation, the value of your savings will halve in about 23 years.

That’s significant, but it’s far from the extremes of your 1977-to-today calculations.

Also, I’m not sure I buy your “deceit” argument. I haven’t seen the government itself doing much in the way of projected savings. But the Retirement Commission, an autonomous crown entity funded by the government, always adjusts for inflation in the KiwiSaver and other calculators on its www.sorted.org.nz website. And below the calculators it explains how inflation affects the numbers.

Note, too, that each year the government adjusts NZ Super for inflation — while also making sure the increases don’t get out of line with wage increases.

A final point: While there’s no doubt that we should take inflation into account, that’s no argument against saving. It would be amazing if returns on KiwiSaver accounts over the years don’t average considerably more than inflation. So people’s savings will still grow in terms of buying power.

QI have been following all your information on KiwiSaver and have noticed you say as a beneficiary on long-term ACC I can pay the minimum ie not 4 per cent of pay.

I have since found out through Inland Revenue, after signing, this is not so. Long-term ACC recipients are not classed as beneficiaries in the case of KiwiSaver.

So then I suggested ACC must be my employer, and I would qualify for employer contributions when they start. “Not so,” is the answer to that. Sounds very confusing and certainly not as straightforward as I had understood it to be. Grrrrrrr.

ACalm down! It’s not relevant whether you are classed as a beneficiary. Inland Revenue has confirmed that you can contribute as little as you like to KiwiSaver, as long as you find a provider that is happy with your contributions.

Actually, ACC recipients have a choice. If you want, you can tell ACC to put 4 or 8 per cent of your payments into your KiwiSaver account. If you do that, your contributions then continue unless you take a contributions holiday. Otherwise, you can simply deal directly with a provider, just like all non-employees.

Whichever way you do it, though, ACC will not make compulsory employer contributions.

Others may want to note that similar rules apply for Paid Parental Leave. You can approach a KiwiSaver provider directly and contribute whatever you wish, or ask Inland Revenue — which pays you the allowance — to put 4 or 8 per cent of your allowance into KiwiSaver. Again, either way, employer contributions don’t apply.

QI have been aiming for an early retirement at age 55, and my savings plans (20–30 per cent of income a year) are geared for it. I hope to live to about 80.

At 55, it will be some 10 years before I could get access to KiwiSaver money. However, given past government’s untrustworthy track record with superannuation, the age of entitlement of 65 may increase to 70 in twenty years time. The fact that it has increased from 60 to 65 in the last twenty adds weight to this possibility).

Diverting and locking up 4 per cent of my income (not insignificant) may impact these plans, delaying my retirement for a couple more years or even to 60, and that will still leave me waiting for 5–10 years before I get access to KiwiSaver.

In addition, if the age of entitlement does change to 70, I will only have 10 years to enjoy the return. What is your view on this?

AYou can still gain plenty by being in KiwiSaver, and it shouldn’t hurt you in any way.

At the very least, you should sign up and contribute to KiwiSaver for a year, to pick up the $1,000 kick-start and one year’s worth of tax credits. If you wish, you can always go on contributions holidays after that.

In your case, though, I don’t see any disadvantage — and a couple of big advantages — in continuing to contribute 4 per cent of your pay to KiwiSaver as long as you are employed. And after retirement you should contribute $1043 a year. The advantages are: the KiwiSaver tax credit and employer contributions.

You’re quite right that a future government might raise the age at which you can get your money out to 70. But that shouldn’t affect you at all.

Regardless of KiwiSaver, if you retire at 55 and expect to live to 80, I would advise you to set aside around a quarter of your nest egg anyway, to cover your expenses from age 70 to 80.

Initially, you might put that money into higher-risk/higher-return investments such as share funds, as you would have 15 to 25 years before you will be spending it. As the spending time approaches, gradually move the money to less volatile investments.

If KiwiSaver gets 4 per cent out of your current savings of 20 to 30 per cent of pay, at 55 your KiwiSaver account will almost certainly hold less than a quarter of your total savings. So having that money tied up until you are 70 shouldn’t pose a problem.

Not convinced? I doubt if the government will mind. You are already saving enough for retirement, and don’t need taxpayer-funded incentives to encourage you. But if I were you I would take my share.

QUICK KIWISAVER INFO

For basic information about KiwiSaver, see the KiwiSaver book page on www.maryholm.com. [This page has been removed from the website. Visit kiwisaver.govt.nz for up-to-date information.]

Other sources of information are the Retirement Commission’s website, www.sorted.org.nz or the government’s www.kiwisaver.govt.nz. Alternatively, call 0800 KiwiSave (0800 549 472, Monday to Friday 8 to 8, or Saturday 9 to 1.

No paywalls or ads — just generous people like you. All Kiwis deserve accurate, unbiased financial guidance. So let’s keep it free. Can you help? Every bit makes a difference.

Mary Holm is a freelance journalist, a director of Financial Services Complaints Ltd (FSCL), a seminar presenter and a bestselling author on personal finance. From 2011 to 2019 she was a founding director of the Financial Markets Authority. Her opinions are personal, and do not reflect the position of any organisation in which she holds office. Mary’s advice is of a general nature, and she is not responsible for any loss that any reader may suffer from following it. Send questions to [email protected] or click here. Letters should not exceed 200 words. We won’t publish your name. Please provide a (preferably daytime) phone number. Unfortunately, Mary cannot answer all questions, correspond directly with readers, or give financial advice.